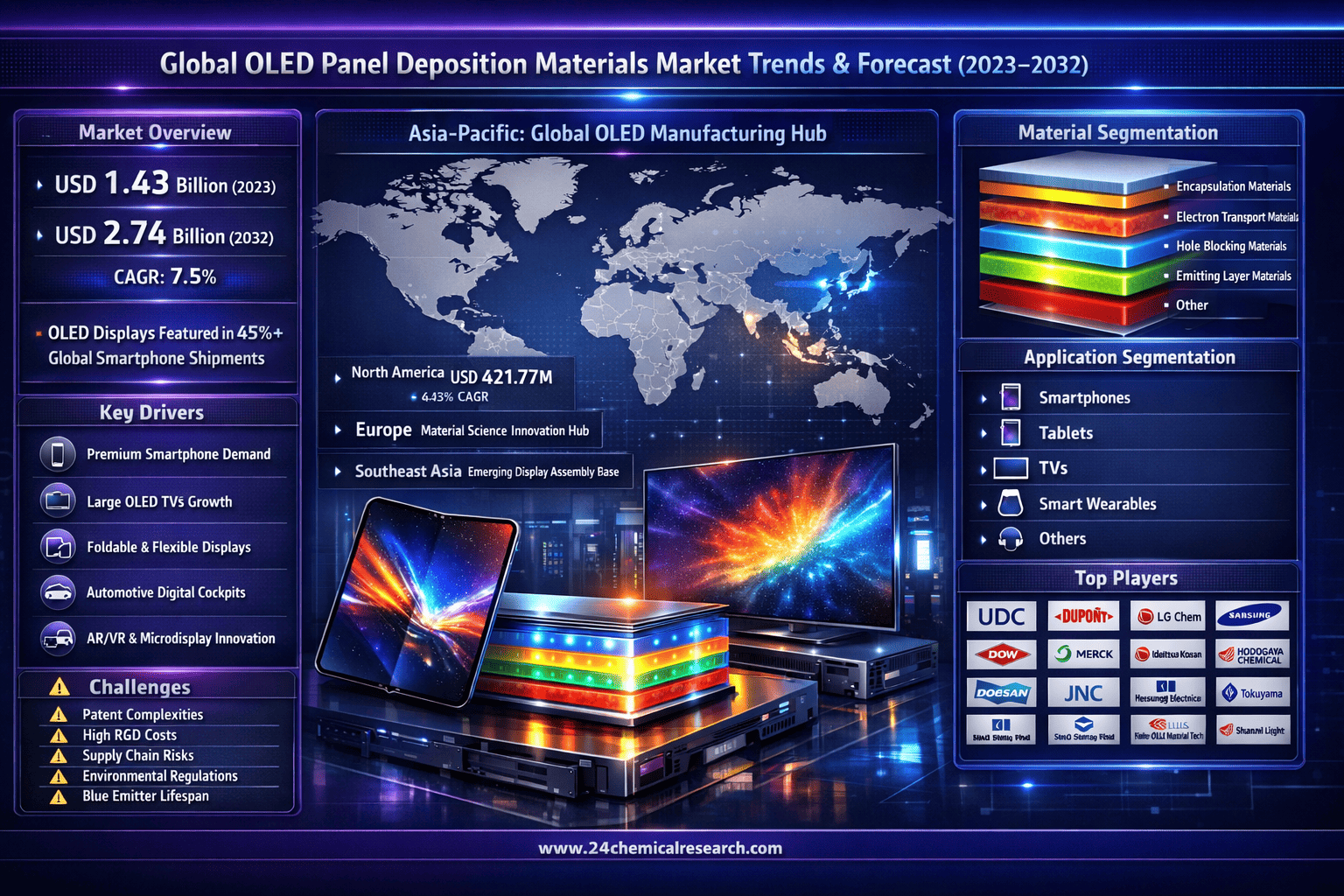

Global OLED Panel Deposition Materials market demonstrates robust expansion, with its valuation reaching USD 1.43 billion in 2023. According to latest industry projections, the market is expected to grow at a CAGR of 7.5%, reaching approximately USD 2.74 billion by 2032. This dynamic growth stems from increasing adoption in consumer electronics and next-generation display technologies, particularly in regions with strong technology manufacturing ecosystems.

OLED deposition materials form the foundation for creating high-performance organic light-emitting diode displays. Their ability to enable thinner, more flexible, and energy-efficient screens makes them indispensable for manufacturers transitioning toward advanced display solutions. As foldable devices and microdisplays gain traction, material innovators and display makers are collaborating to push performance boundaries.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/282696/global-oled-panel-deposition-materials-market-2025-2032-442

Market Overview & Regional Analysis

Asia-Pacific commands over 75% of global OLED material production, with South Korea, Japan, and China forming the industry's manufacturing backbone. The region benefits from established display panel manufacturing clusters, substantial R&D investments, and strong government support for display technology development. North America's market, valued at USD 421.77 million in 2023, grows steadily at 6.43% CAGR through 2032, driven by specialty applications in defense and medical equipment.

Europe maintains technological leadership in material science innovation, particularly in Germany and the UK, while facing challenges in scaling production capacities. Emerging markets in Southeast Asia show increasing potential as display assembly operations decentralize from traditional manufacturing hubs.

Key Market Drivers and Opportunities

The market thrives on surging demand for high-end smartphones, with OLED displays now featured in over 45% of global shipments. The television sector presents significant growth potential as large-format OLED TVs gain consumer acceptance. Emerging applications in automotive displays, augmented reality devices, and flexible electronics are creating new material requirements that manufacturers are actively addressing. With display technology advancing toward higher resolutions and brightness levels, material developers face both challenges and opportunities in meeting these evolving specifications.

Strategic opportunities exist in developing materials for quantum dot-OLED hybrids and improving the lifetime of blue OLED emitters—two areas where significant industry R&D resources are currently focused.

Challenges & Restraints

The OLED materials sector faces hurdles including complex patent landscapes, high R&D costs for new formulations, and stringent purity requirements. Supply chain vulnerabilities, particularly for rare-earth elements used in some emissive materials, continue to pose production risks. Environmental regulations regarding chemical usage in manufacturing processes are becoming increasingly rigorous, requiring material suppliers to invest in cleaner production methods.

Market Segmentation by Type

-

Encapsulation Layer Materials

-

Electron Transport Layer Materials

-

Hole Blocking Layer Materials

-

Emitting Layer Materials

-

Other

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/282696/global-oled-panel-deposition-materials-market-2025-2032-442

Market Segmentation by Application

-

Smartphones

-

Tablets

-

TVs

-

Smart Wearable Devices

-

Others

Market Segmentation and Key Players

-

UDC

-

DuPont

-

LG Chem

-

Samsung SDI

-

DOW

-

Merck

-

Idemitsu Kosan

-

Hodogaya Chemical

-

Doosan

-

JNC CORPORATION

-

Heesung Electronics

-

Tokuyama

-

Materion

-

Changchun Hyperions Technology

-

Jilin OLED Material Tech

-

Shaanxi Lighte Optoelectronics Material

Report Scope

This report provides comprehensive analysis of the global OLED Panel Deposition Materials market from 2024 through 2032, featuring detailed regional breakdowns and technology trends. The research focuses on:

-

Material demand forecasts by application segment

-

Technology adoption timelines across different display generations

The study includes in-depth profiles of leading market participants, covering:

-

Product portfolios and patent positions

-

Production capacities and expansion plans

-

Strategic partnerships and customer relationships

-

Financial performance and R&D investment trends

Our research methodology combines supplier interviews with end-user surveys across the display supply chain, evaluating:

-

Material performance requirements for next-gen applications

-

Adoption barriers and technology pain points

-

Emerging material alternatives and substitution risks

Get Full Report Here: https://www.24chemicalresearch.com/reports/282696/global-oled-panel-deposition-materials-market-2025-2032-442

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch