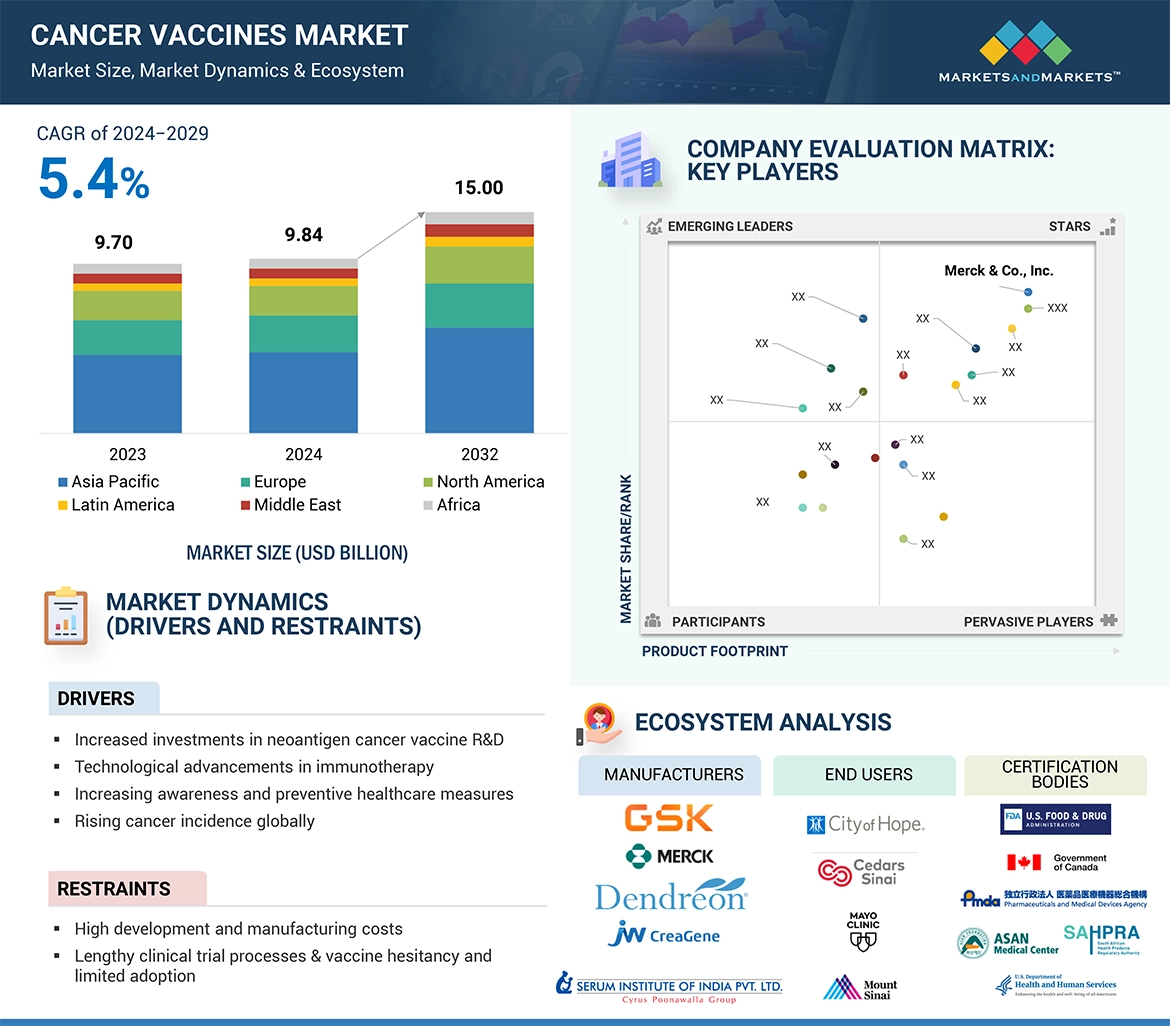

The global cancer vaccines market is entering a period of robust, sustained expansion — driven by a convergence of immunological breakthroughs, rising cancer incidence, and the accelerating adoption of precision medicine. According to the Cancer Vaccines Market report by MarketsandMarkets, valued at US$9.70 billion in 2023, the market climbed to US$9.84 billion in 2024 and is forecast to grow at a compound annual growth rate (CAGR) of 5.4% between 2024 and 2032, culminating in a projected valuation of US$15.00 billion by the end of the period.

📊 Full Market Report Available

Access in-depth data, forecasts, and competitive intelligence from MarketsandMarkets.

Market Overview

Cancer vaccines represent one of the most dynamic frontiers in oncology, spanning two primary categories: prophylactic (preventive) vaccines that guard against cancer-causing pathogens, and therapeutic vaccines that train the immune system to recognize and destroy existing tumor cells. Both segments are benefiting from decades of immunological research now reaching clinical and commercial maturity.

Unlike conventional vaccines, therapeutic cancer vaccines are highly personalized — often designed around a patient's unique tumor antigens. This personalized medicine paradigm, powered by next-generation sequencing and mRNA technology, is one of the most compelling forces shaping the market's near-term trajectory.

"The mRNA revolution ignited by COVID-19 vaccines has dramatically accelerated the development pipeline for therapeutic cancer vaccines — bringing treatments once considered futuristic into imminent clinical reach."

Key Market Drivers

1. Rising Global Cancer Burden

Cancer remains a leading cause of death worldwide, with the World Health Organization estimating over 20 million new cases annually. As population aging and lifestyle-related risk factors continue to drive incidence rates upward, the demand for effective prophylactic and therapeutic interventions — including vaccines — intensifies correspondingly.

2. Breakthroughs in mRNA Technology

The success of mRNA-based COVID-19 vaccines galvanized investment and regulatory confidence in mRNA platforms. Companies such as Moderna and BioNTech are now advancing mRNA-based personalized cancer vaccines through late-stage clinical trials. These vaccines can be tailored to a patient's individual tumor mutational landscape, offering unprecedented specificity in immune targeting.

3. Expanding Prophylactic Vaccine Adoption

HPV vaccines — particularly Gardasil and Cervarix — continue to see growing uptake across developed and developing markets alike, driven by expanded national immunization programs. Gardasil 9 protects against nine HPV strains and now addresses cancers of the cervix, vulva, vagina, penis, anus, and oropharynx.

4. Favorable Regulatory Environment

Regulatory agencies including the U.S. FDA and EMA have extended Breakthrough Therapy and Fast Track designations to numerous cancer vaccine candidates, compressing development timelines and incentivizing investment.

5. Growing Investment in Oncology R&D

Global pharmaceutical and biotechnology companies are allocating record R&D budgets to oncology, with cancer vaccines occupying a growing share. Collaborations between academic research institutions, government bodies, and private-sector players are generating an increasingly rich clinical pipeline.

Market Challenges & Restraints

- High Development Costs: Personalized therapeutic vaccines are capital-intensive, limiting near-term accessibility to high-income markets.

- Regulatory Complexity: Personalized vaccines create challenges around standardization, trial design, and approval pathways.

- Limited Awareness in LMICs: Prophylactic vaccine adoption in low- and middle-income countries remains constrained by cost and supply chain gaps.

- Efficacy Variability: Immune response variability among patients creates challenges in demonstrating consistent clinical efficacy.

Market Segmentation

By Type

| Vaccine Type | Description | Key Examples |

|---|---|---|

| Prophylactic | Prevents cancer by targeting oncogenic pathogens | Gardasil (HPV), Hepatitis B vaccine |

| Therapeutic | Treats existing cancer via immune activation | Provenge (sipuleucel-T), mRNA-4157 |

By Technology

| Technology | Market Stage |

|---|---|

| Recombinant Protein / Subunit | Established / Commercial |

| Whole Cell / Lysate | Established / Clinical |

| Dendritic Cell-Based | Approved (Provenge) |

| mRNA-Based | Late-Stage Clinical |

| Viral Vector | Clinical / Emerging |

| DNA-Based | Early Clinical |

| Peptide-Based | Clinical / Emerging |

By Cancer Indication

- Cervical Cancer (HPV-driven; largest prophylactic segment)

- Prostate Cancer (sipuleucel-T; most established therapeutic segment)

- Lung Cancer (active mRNA & checkpoint-adjuvant pipeline)

- Melanoma (BNT111 and mRNA-4157 in late-stage trials)

- Colorectal, Breast, and Bladder Cancers (growing pipeline)

Regional Analysis

North America — Market Leader

North America commands the largest share of the global cancer vaccines market, underpinned by advanced healthcare infrastructure, high R&D investment, and strong HPV vaccination coverage.

Europe — Strong Innovation Hub

Europe is the second-largest regional market, with Germany, France, and the UK leading in R&D output and immunization program breadth.

Asia Pacific — Fastest-Growing Region

Asia Pacific is projected to register the highest CAGR over the forecast period, driven by HPV program expansion in China and India, and domestic R&D growth in Japan and South Korea.

Latin America & MEA — Emerging Opportunities

These regions remain at an earlier stage but hold significant long-term potential as cervical cancer incidence remains elevated and governments invest in preventive healthcare infrastructure.

Pipeline Highlights: Vaccines to Watch

- mRNA-4157 / V940 (Moderna + Merck): Personalized neoantigen vaccine combined with pembrolizumab — Phase 3 for melanoma.

- BNT111 (BioNTech): mRNA-based vaccine targeting four melanoma-associated antigens; Phase 2 results promising.

- ATLAS / NeoVax (Neon Therapeutics / Dana-Farber): Neoantigen vaccine platform with trials in melanoma and glioblastoma.

- CV301 (Bavarian Nordic): MVA-based vaccine targeting CEA and MUC1 in colorectal and breast cancers.

- DCVAC/PCa (Sotio): Dendritic cell vaccine for prostate cancer; Phase 3 ongoing in Europe.

Competitive Landscape

- Merck & Co. — Gardasil franchise; mRNA-4157 partnership with Moderna

- Moderna, Inc. — Leading mRNA therapeutic cancer vaccine pipeline

- BioNTech SE — Individualized neoantigen therapy program

- Bristol-Myers Squibb — Cancer vaccine + checkpoint inhibitor combinations

- Bavarian Nordic — Viral-vector cancer vaccine platform

- Dendreon (Valeant) — Provenge, the first FDA-approved therapeutic cancer vaccine

- GSK plc — Cervarix HPV vaccine; adjuvant technology leadership

"Strategic alliances between mRNA biotech firms and established oncology players are redefining the competitive architecture of cancer vaccine development — collapsing timelines that once spanned decades."

Market Outlook: 2024–2032

- Anticipated approval of one or more mRNA-based personalized cancer vaccines within 3–4 years

- Expanded WHO and UNICEF-supported HPV vaccination programs in LMICs

- Growing adoption of cancer vaccines combined with immune checkpoint inhibitors

- Continued reduction in neoantigen sequencing and manufacturing costs

- Increased investment following COVID-19-driven validation of mRNA platforms

With a CAGR of 5.4% and a clear path to US$15.00 billion by 2032, the cancer vaccines market represents one of the most compelling growth opportunities in global biopharmaceuticals.

Conclusion

Cancer vaccines are transitioning from a niche immunological concept to a mainstream pillar of oncology care. The convergence of mRNA technology maturity, expanding clinical pipelines, supportive regulatory frameworks, and a surging global cancer burden positions the market for durable, multi-decade growth.

Source:Cancer Vaccines Market — Size, Share & Industry Analysis | MarketsandMarkets. For the complete report, download the PDF brochure here.

Table of Contents

Key Statistics

| 2023 Value | US$9.70B |

| 2024 Value | US$9.84B |

| 2032 Forecast | US$15.00B |

| CAGR | 5.4% |

📄 Research Report

Get the complete cancer vaccines market analysis — forecasts, segments, players, and more.

View Full Report →⬇ Download PDF BrochureRelated Tags

© 2025 Market Research Insights · Cancer Vaccines Market Report · All rights reserved

This article is intended for informational and off-page SEO distribution purposes.