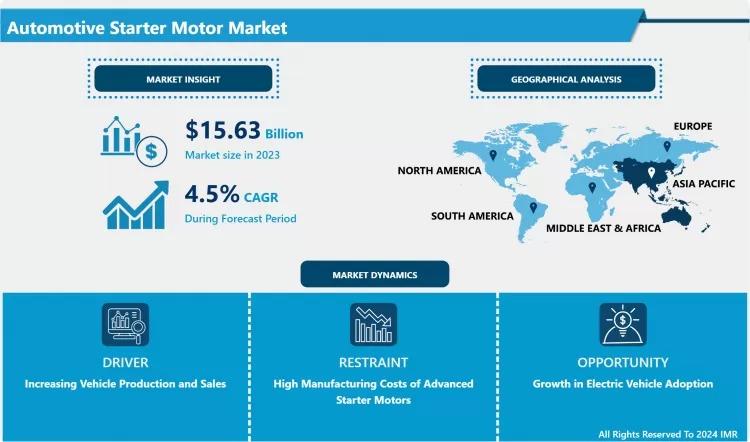

According to a new report published by Introspective Market Research, Automotive Starter Motor Market by Vehicle Type, Technology, and Sales Channel, The Global Automotive Starter Motor Market Size Was Valued at USD 15.63 Billion in 2023 and is Projected to Reach USD 22.22 Billion by 2032, Growing at a CAGR of 4.50%.

Market Overview

Automotive starter motors are essential components in internal combustion engine (ICE) vehicles, responsible for initiating engine operation by converting electrical energy from the battery into mechanical energy. These motors play a critical role in vehicle ignition systems and are widely used in passenger cars, commercial vehicles, and light-duty trucks. Modern starter motors are designed for enhanced durability, compact size, and improved torque output, ensuring reliable engine performance under varying operating conditions.

Growth Driver:

One of the primary growth drivers of the automotive starter motor market is the sustained production and sales of internal combustion engine vehicles worldwide. Emerging economies continue to experience rising vehicle ownership due to urbanization, infrastructure development, and increasing disposable incomes. Additionally, the growing adoption of start-stop technology to improve fuel efficiency and reduce carbon emissions has increased demand for advanced and durable starter motors. Stringent government regulations aimed at lowering vehicle emissions have encouraged automakers to integrate energy-efficient starter systems, thereby supporting consistent market growth.

Market Opportunity:

A significant market opportunity lies in technological advancements and hybrid vehicle integration. While fully electric vehicles do not require traditional starter motors, hybrid vehicles still rely on modified starter-generator systems. This opens avenues for innovation in lightweight, high-efficiency, and compact starter motor designs. Furthermore, the expanding automotive aftermarket sector presents growth opportunities due to rising vehicle age and maintenance requirements. Manufacturers focusing on durable, cost-effective, and high-performance starter motors can capitalize on replacement demand, particularly in developing regions with growing automotive fleets.

The Automotive Starter Motor Market is segmented on the basis of Vehicle Type, Technology, and Sales Channel.

Vehicle Type

The Vehicle Type segment is further classified into Passenger Vehicles, Commercial Vehicles, and Light Commercial Vehicles. Among these, the Passenger Vehicles sub-segment accounted for the highest market share in 2023. The dominance of passenger vehicles is attributed to their high production volumes and increasing consumer demand worldwide. Rapid urbanization and rising middle-class populations have significantly boosted passenger car sales, particularly in Asia-Pacific. Additionally, the integration of start-stop systems in modern passenger cars has increased the need for high-performance starter motors capable of handling frequent ignition cycles, further strengthening this segment’s leading position.

Technology

The Technology segment is further classified into Direct Drive, Gear Reduction, and Start-Stop Systems. Among these, the Gear Reduction sub-segment accounted for the highest market share in 2023. Gear reduction starter motors offer higher torque output while being smaller and lighter than direct-drive variants. Their improved efficiency and reduced power consumption make them suitable for modern vehicles requiring compact engine designs. Automakers prefer gear reduction technology due to its durability, enhanced performance in cold-start conditions, and compatibility with fuel-efficient engine systems, contributing to its market leadership.

Some of The Leading/Active Market Players Are-

- Robert Bosch GmbH (Germany)

• Denso Corporation (Japan)

• Valeo SA (France)

• Mitsubishi Electric Corporation (Japan)

• Hitachi Astemo Ltd. (Japan)

• BorgWarner Inc. (USA)

• Mahle GmbH (Germany)

• ZF Friedrichshafen AG (Germany)

• Hella GmbH & Co. KGaA (Germany)

• Lucas TVS Ltd. (India)

• Prestolite Electric Incorporated (USA)

• Remy International Inc. (USA)

• ASIMCO Technologies Ltd. (China)

and other active players.

Key Industry Developments

News 1:

In January 2024, a leading automotive component manufacturer introduced a new lightweight gear reduction starter motor designed for fuel-efficient passenger vehicles.

The product aims to improve torque performance while reducing overall vehicle weight. This development supports automakers in meeting stringent emission norms and enhancing engine efficiency across compact and mid-sized vehicle segments.

News 2:

In August 2023, a global automotive supplier expanded its manufacturing facility in Asia-Pacific to strengthen starter motor production capacity.

The expansion focuses on meeting rising regional demand and supporting OEM partnerships. Increased localization is expected to reduce production costs and enhance supply chain efficiency for automotive manufacturers.

Key Findings of the Study

- Passenger vehicles dominated the market in 2023.

• Gear reduction technology held the largest share.

• Asia-Pacific remains the leading regional market.

• Rising ICE vehicle production drives demand.

• Start-stop systems enhance growth prospects.