According to 24Chemical Research, Global Dead-burned Dolomite market was valued at USD million in 2023 and is projected to reach USD million by 2030, exhibiting a compound annual growth rate (CAGR) of % during the forecast period.

Dead-burned dolomite, a calcined form of dolomitic limestone processed at high temperatures (1500-2000°C), has transformed from a basic refractory material to a critical industrial mineral. Its superior thermal stability, high magnesium oxide content, and excellent resistance to basic slags make it indispensable across multiple heavy industries. Unlike raw dolomite, the dead-burned variant demonstrates enhanced physical properties including higher density (2.8-3.0 g/cm³) and superior refractory characteristics that withstand temperatures exceeding 1800°C.

Get Full Report Here: https://www.24chemicalresearch.com/reports/265350/global-deadburned-dolomite-market-2024-2030-735

Market Dynamics:

The dead-burned dolomite market navigates a complex matrix of industrial demand drivers, technical constraints, and emerging technological opportunities that are reshaping its global trajectory.

Dominant Market Drivers Accelerating Growth

-

Steel Industry's Insatiable Demand: The steel sector consumes approximately 60% of global dead-burned dolomite production, primarily as a refractory lining material in basic oxygen furnaces and electric arc furnaces. With global crude steel output exceeding 1.8 billion metric tons annually, even incremental efficiency improvements in refractory life (typically 300-500 heats per lining) drive significant material consumption. Emerging steelmaking technologies like twin-shell EAFs are increasing dolomite usage by 15-20% per unit of steel produced.

-

Cement Industry's Shift Toward Sustainable Practices: Dead-burned dolomite is gaining traction as a supplementary cementitious material, particularly in magnesium oxychloride cement formulations. These specialty cements demonstrate 30-40% lower carbon emissions compared to Portland cement and superior fire resistance. The global push for green building materials is creating a new demand stream, especially in European and North American construction markets.

-

Agriculture's Magnesium Correction Needs: The increasing magnesium deficiency in arable soils (affecting over 50% of agricultural land globally) is driving adoption of dolomitic soil conditioners. Dead-burned dolomite's slow-release magnesium and calcium ions improve soil structure better than raw dolomite, with application rates ranging 1-5 tons per acre depending on soil conditions.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/265350/global-deadburned-dolomite-market-2024-2030-735

Significant Market Constraints Impacting Adoption

While the market shows strong growth potential, several barriers require strategic solutions for broader industry adoption.

-

Energy-Intensive Production Process: The dead-burning process consumes 1.8-2.5 MWh per ton of product, making energy costs account for 35-45% of total production expenses. In regions with high electricity prices, this creates a 20-30% cost disadvantage compared to alternative refractory materials. Recent energy price volatility has forced some European producers to operate at just 60-70% capacity.

-

Technical Limitations in High-Stress Applications: While excellent for basic steelmaking environments, dead-burned dolomite performs poorly in acidic or variable pH conditions. Its hydration tendency limits use in humid environments unless specially treated, adding 10-15% to material costs. In aluminum production furnaces, for instance, dolomite linings last only half as long as premium alumina-based alternatives.

Critical Operational Challenges in the Value Chain

The industry faces several production and logistical hurdles that impact profitability and market expansion.

Maintaining consistent quality from variable dolomite deposits remains problematic, with impurity levels (particularly silica and iron oxides) varying 3-8% between batches. This necessitates costly blending operations to meet the <1.5% silica specification preferred by refractory manufacturers. Transportation presents another challenge—dead-burned dolomite's bulk density of 1.5-1.8 t/m³ makes long-distance shipping economically viable only for premium applications, limiting penetration in emerging markets.

Additionally, the industry contends with environmental compliance costs. Modern rotary kilns require sophisticated emission control systems (representing 15-20% of capital costs) to meet particulate matter standards below 30 mg/Nm³ in developed markets. The shift from natural gas to alternative fuels in calcination also presents technical challenges—biomass fuels, while reducing carbon footprint by 40%, often create inconsistent thermal profiles that impact product quality.

Emerging Market Opportunities Creating New Pathways

-

Circular Economy Applications: Innovative uses in waste remediation are gaining traction, particularly for treating acidic mine drainage where dead-burned dolomite's high surface reactivity neutralizes pH 3-4 solutions 50% faster than limestone. Pilot projects in Canadian and Chilean mines demonstrate 80-90% heavy metal removal at half the operating cost of conventional lime treatments.

-

Advanced Refractory Composites: Material science breakthroughs are enabling dolomite-magnesia-alumina spinel compositions that extend refractory life in steel ladles by 30-40%. Japanese and German manufacturers are leading this innovation, with new formulations commanding 25-35% price premiums over conventional dolomite bricks.

-

Strategic Vertical Integration: Leading producers are securing long-term raw material access through mine-to-market strategies. Grecian Magnesite's acquisition of a Brazilian dolomite deposit in 2023 exemplifies this trend, ensuring supply security while reducing logistical costs by 18-22% for South American customers.

In-Depth Segment Analysis: Key Market Divisions

By Type:

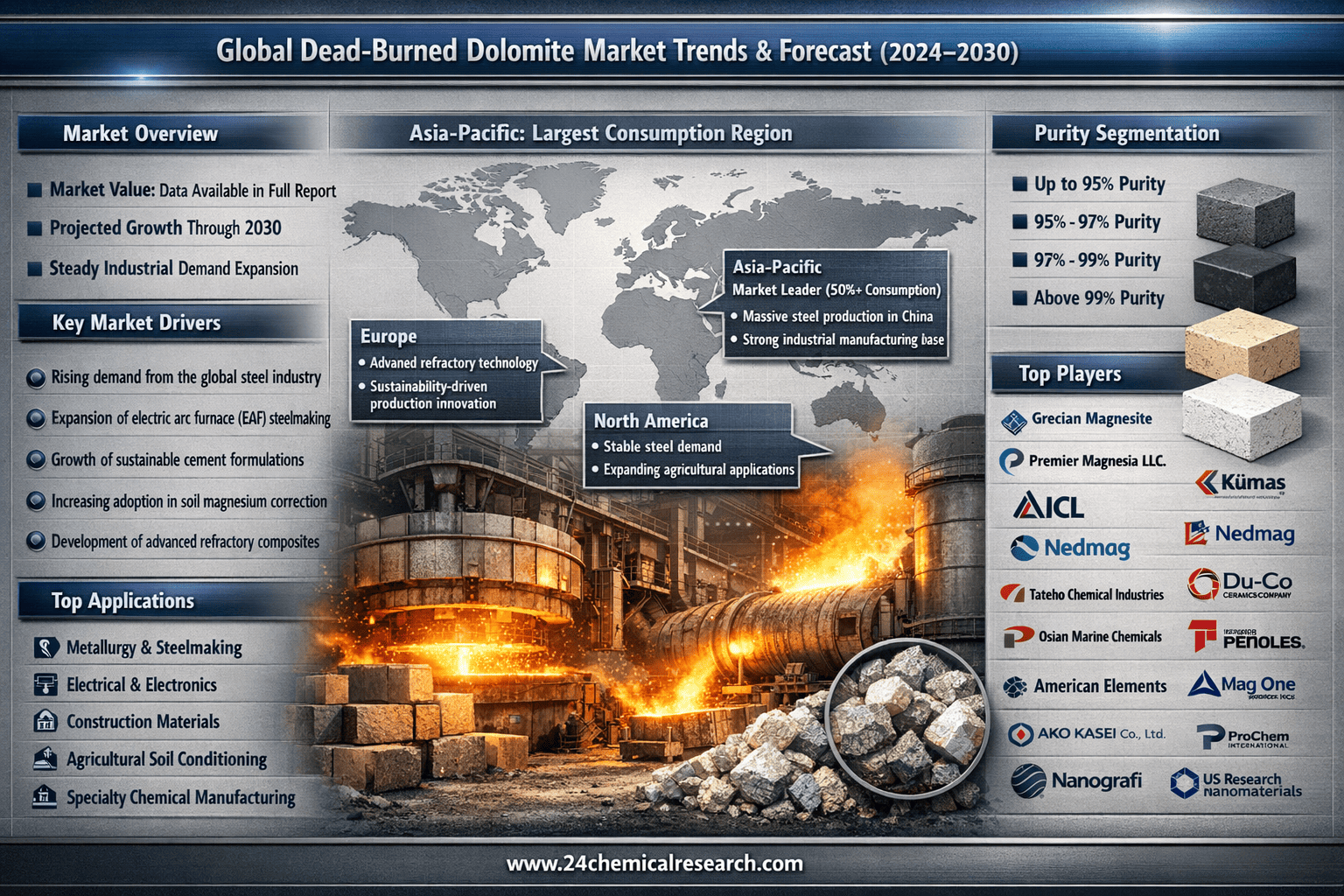

The market is segmented by purity levels: Up to 95%, 95% to 97%, 97% to 99%, and Above 99%. The 95% to 97% purity segment currently dominates industrial applications, offering the optimal balance between cost and performance for most refractory uses. Higher purity grades (Above 99%) are reserved for specialty applications like optical grade magnesium production, where even minor impurities can affect product quality.

By Application:

Key application areas include Metallurgy, Electrical and Electronics, Construction, Agriculture, Pharmacy, and Others. The Metallurgy sector commands the largest share, consuming over 60% of production primarily for steelmaking refractories. However, Construction applications are growing fastest, particularly for fire-resistant building materials in seismic zones where dolomite-based products provide better crack resistance than conventional materials.

By End-User Industry:

The end-user landscape spans Steel, Cement, Chemicals, Agriculture, and Specialty Manufacturing. Steel producers remain the cornerstone consumers, but the Chemicals industry is emerging as a significant growth sector, particularly for magnesium compound production where dead-burned dolomite serves as a preferred feedstock due to its consistent composition.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/265350/global-deadburned-dolomite-market-2024-2030-735

Competitive Landscape:

The global dead-burned dolomite market features a mix of large multinational mineral companies and regional specialists. The top players—Grecian Magnesite, Premier Magnesia, and ICL—collectively control about 45% of global production capacity. Their market position stems from integrated operations combining mining, processing, and distribution networks. Smaller players compete through niche applications or regional proximity to customer bases, particularly in Asia where local dolomite quality variations favor domestic producers.

List of Key Dead-burned Dolomite Companies Profiled:

-

Grecian Magnesite (Greece)

-

Premier Magnesia, LLC (USA)

-

Kimas Manyezit Sanayi A.S. (Turkey)

-

ICL (Israel)

-

Nedmag B.V. (Netherlands)

-

Tateho Chemical Industries Co. Ltd. (Japan)

-

Du-Co Ceramics Company (USA)

-

Osian Marine Chemicals Pvt. Ltd. (India)

-

Industrias Penoles (Mexico)

-

American Elements (USA)

-

Mag One Products Inc. (Canada)

-

AKO KASEI co., LTD. (Japan)

-

ProChem, Inc. International (USA)

-

Nanografi Nano Technology (Turkey)

-

US Research Nanomaterials, Inc. (USA)

Competitive differentiation increasingly hinges on sustainability credentials, with leaders investing in solar calcination technologies and carbon capture systems to meet tightening environmental standards in key markets. Product development focuses on value-added formulations—surface-treated dolomite for improved hydration resistance and micronized grades for specialty chemical applications command 20-30% price premiums over standard products.

Regional Market Perspectives

-

Asia-Pacific: Dominates global consumption with over 50% market share, driven by China's massive steel industry which operates more than 1,000 basic oxygen furnaces. Regional production struggles to meet demand, creating import opportunities from Turkey and European suppliers. Japan and South Korea represent premium markets, with strict quality specifications for their advanced steelmaking processes.

-

Europe: Mature but technologically advanced market where environmental regulations are reshaping production. The EU's Carbon Border Adjustment Mechanism is prompting local producers to invest in low-emission kiln technologies, with several plants transitioning to hydrogen fuel trials. Germany and Italy remain consumption leaders, particularly for high-purity grades used in magnesium metal production.

-

North America: Characterized by stable demand from a consolidating steel industry and growing agricultural applications. U.S. producers benefit from abundant natural gas supplies for kiln operations, maintaining cost competitiveness. Mexican cement manufacturers are emerging as significant consumers for specialty dolomite in magnesium phosphate cement formulations.

Get Full Report Here: https://www.24chemicalresearch.com/reports/265350/global-deadburned-dolomite-market-2024-2030-735

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/265350/global-deadburned-dolomite-market-2024-2030-735

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/