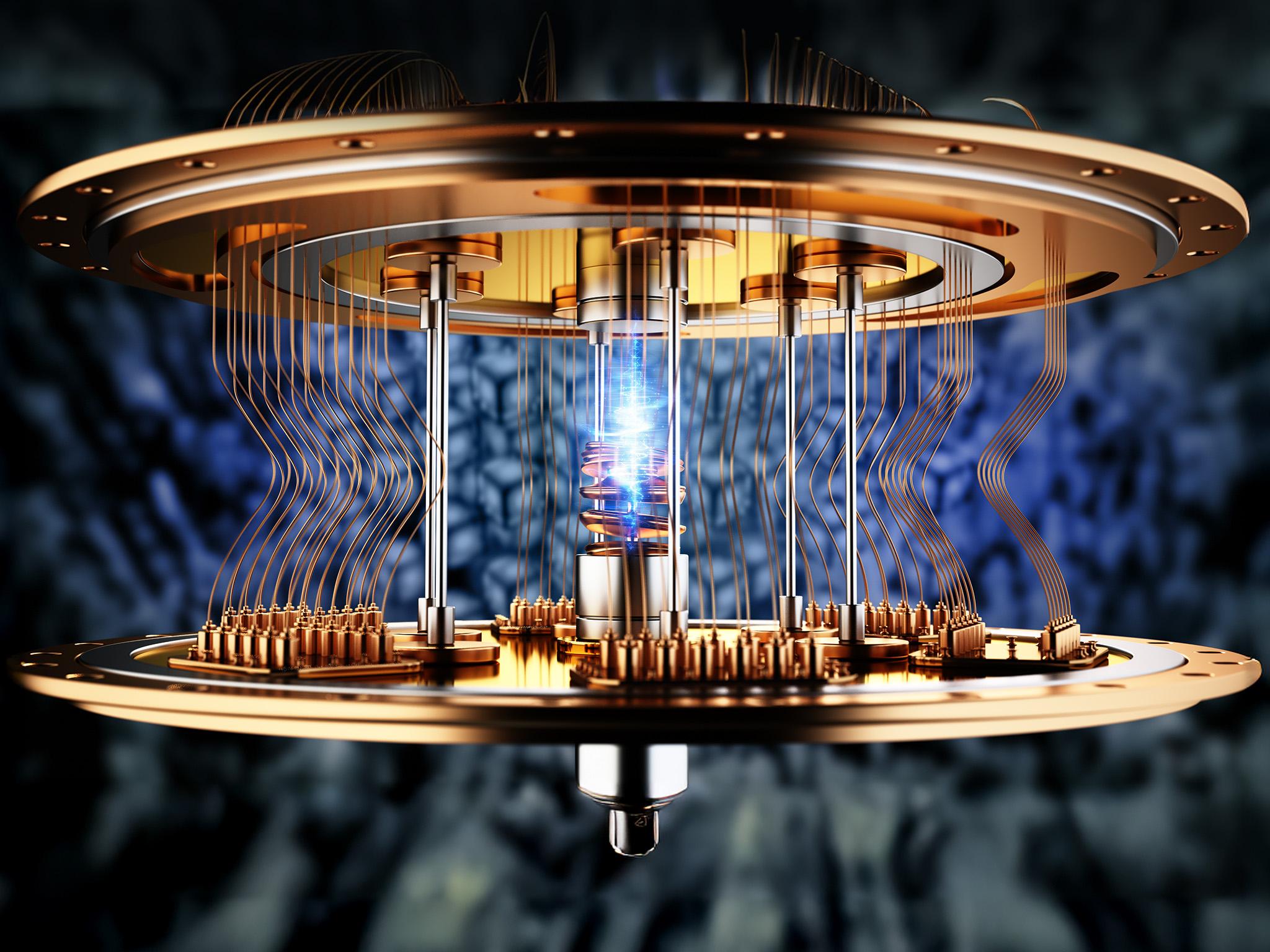

The development of the quantum computing industry is fundamentally a story of hardware innovation, with a diverse and highly competitive race underway to build the most stable, scalable, and high-fidelity quantum bits, or qubits. A hardware-focused market analysis of the Quantum Computing Market reveals several leading physical modalities, each with its own set of advantages and challenges. A key point related to the Quantum Computing Market is that there is no single consensus on which qubit technology will ultimately win out. The most mature and heavily funded approach is based on superconducting circuits, championed by key players like Google and IBM, both based in North America. These qubits offer fast processing speeds but require extreme cryogenic cooling to function, making the systems large and complex. Another leading modality is trapped-ion technology, commercialized by key players such as IonQ (North America) and Quantinuum (a US/UK entity). Trapped-ion qubits boast exceptional stability and long coherence times, leading to higher fidelity, but have historically had slower gate speeds. The future in the Quantum Computing Market will be determined by which of these technologies can best solve the immense engineering challenges of scaling to millions of high-quality qubits, a race keenly watched by researchers in Europe and APAC.

The competitive landscape of quantum hardware is a hotbed of innovation beyond the two leading modalities. A key point is the diversity of approaches being pursued, which mitigates the risk of the entire industry being dependent on a single technological path. Photonic quantum computing, being developed by key players like PsiQuantum in North America and Xanadu in Canada, uses individual particles of light (photons) as qubits. This approach has the significant advantage of potentially operating at room temperature and leverages the mature semiconductor manufacturing ecosystem of regions like APAC. Another promising technology is neutral atoms, where companies like Atom Computing (North America) and Pasqal (Europe) use lasers to arrange hundreds or even thousands of neutral atoms into a qubit array, offering a path to rapid scaling. Silicon quantum dots, which aim to create qubits within the standard silicon architecture of the classical computer industry, are another area of intense research, with strong academic and corporate efforts in Europe and North America. The future in the Quantum Computing Market will likely involve a multi-modal approach, with different hardware types being suited for different kinds of problems. The Quantum Computing Market size is projected to grow USD 14.19 Billion by 2035, exhibiting a CAGR of 27.04% during the forecast period 2025-2035. The developing tech sectors in South America and the MEA are positioning themselves to adopt whichever technology proves most commercially viable.

The strategic goal for all these hardware key players is to create a processor that can support quantum error correction (QEC). A key point is that today's "physical qubits" are too noisy and error-prone for complex computations. The future in the Quantum Computing Market depends on using many of these physical qubits to encode the information of a single, robust "logical qubit" that is resistant to errors. The hardware modality that can demonstrate the most efficient and scalable path to creating high-fidelity logical qubits will likely gain a dominant market position. This is a monumental engineering challenge that requires not just increasing the number of qubits, but also improving their quality (coherence times, gate fidelities) and their connectivity. The regional strengths are distinct: North America leads in superconducting and has strong players across the board; Europe has deep research strengths in silicon and photonics; and APAC's manufacturing prowess could be a major advantage for modalities like photonics in the long term. This hardware race is the foundational element that will dictate the timeline for practical quantum computing.

In summary, key points related to the hardware landscape highlight a vibrant, multi-modal competition to build the fundamental unit of quantum computation. The market features key players from big tech and specialized startups, each betting on a different physical approach, from superconducting circuits and trapped ions to photonics and neutral atoms. The future in the Quantum Computing Market is a race not just for more qubits, but for higher-quality, error-corrected logical qubits. This global R&D effort, centered in North America, Europe, and an increasingly ambitious APAC, with future adoption expected in South America and the MEA, will determine the timeline for when quantum computing's full potential can be realized. The outcome of this hardware race will have profound implications for all other segments of the quantum ecosystem.

Top Trending Reports -

France Corporate E-Learning Industry